Have you ever received an SMS, email, or app notification saying “You are pre-approved for a credit card”? Many people assume these offers are random marketing messages, but in reality banks use advanced data analysis and credit profiling to carefully select eligible customers.

In 2026, pre-approved credit card offers have become one of the fastest ways to get a credit card with instant approval, minimal documentation, and higher acceptance chances. This guide explains how banks choose you, how pre-approved offers work, and how to improve your chances of receiving one.

What Is a Pre-Approved Credit Card Offer?

A pre-approved credit card is an offer given by a bank after evaluating your financial profile in advance. Unlike normal applications, the bank has already assessed your eligibility before you apply.

Key Features:

- Higher approval probability

- Minimal documentation required

- Faster processing time

- Often instant digital approval

- Sometimes lifetime free or special rewards

However, “pre-approved” does not always mean guaranteed approval. Final verification still happens before card issuance.

How Banks Select Customers for Pre-Approved Credit Cards

Banks use automated risk assessment systems powered by credit bureau data and internal banking analytics.

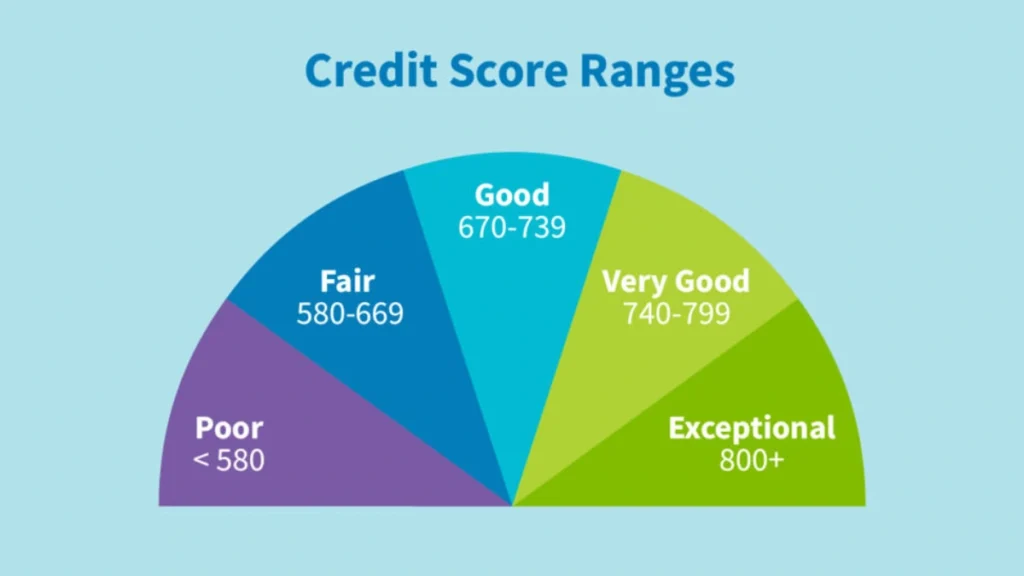

1. Credit Score (CIBIL Score)

Your credit score is the most important factor.

Typical selection range:

- 750+ score: High chance of premium offers

- 700+ score: Standard cashback or rewards cards

- Below 650: Rarely pre-approved

A strong repayment history signals low risk to lenders.

2. Existing Relationship with the Bank

Banks prefer customers they already know.

You are more likely to receive offers if you:

- Maintain a salary account

- Have savings or fixed deposits

- Use debit cards frequently

- Have existing loans with timely payments

Internal banking data helps lenders evaluate your financial behavior.

3. Income Stability and Cash Flow

Banks analyze transaction patterns instead of only salary slips.

They look for:

- Regular monthly credits

- Stable account balance

- Consistent spending behavior

- Low cheque bounce history

Stable income flow increases trust.

4. Credit Usage Behavior

Banks review how you manage existing credit products.

Positive indicators:

- Low credit utilization (below 30%)

- On-time EMI payments

- Long credit history

- No loan defaults

Responsible credit usage increases chances of pre-approved offers.

5. Spending Pattern Analysis (AI-Based Selection)

In 2026, banks use AI models to predict customer spending habits.

Examples:

- Frequent online shopping → Cashback cards

- Travel spending → Travel rewards cards

- Utility payments → Lifestyle cards

This is why many offers feel “personalized.”

6. Employer Profile and Job Stability

Banks also consider risk based on employer category.

Preferred profiles:

- Government employees

- MNC workers

- Stable private sector professionals

Longer employment duration improves eligibility.

Types of Pre-Approved Credit Card Offers

✔ Lifetime Free Card Offers

No joining or annual fees for selected customers.

✔ Upgrade Offers

Existing cardholders receive higher-limit or premium cards.

✔ Instant Digital Cards

Virtual cards issued immediately after acceptance.

✔ Co-Branded Offers

Amazon, Flipkart, or travel partner credit cards based on spending data.

Benefits of Pre-Approved Credit Cards

- Faster approval compared to normal applications

- Reduced paperwork

- Higher credit limits

- Exclusive welcome benefits

- Better reward structures

Many users receive card approval within minutes after accepting the offer.

How to Increase Chances of Getting Pre-Approved Offers

Follow these proven strategies:

- Maintain CIBIL score above 750

- Use debit card regularly

- Keep salary account active

- Avoid missed payments

- Maintain stable bank balance

- Limit multiple loan inquiries

Banks continuously scan customer databases, so improving financial habits automatically increases eligibility.

Common Myths About Pre-Approved Offers

Myth 1: Approval Is Guaranteed

Final verification still happens before card issuance.

Myth 2: Offers Affect Credit Score

Receiving offers does not impact your credit score unless you formally apply.

Myth 3: Only High-Income Users Get Offers

Even moderate-income users receive offers if financial behavior is strong.

Things to Check Before Accepting an Offer

Always review:

- Annual fees and hidden charges

- Interest rates

- Reward redemption rules

- Cashback caps

- Joining conditions

Never accept an offer without reading terms carefully.

Frequently Asked Questions (FAQs)

Are pre-approved credit cards guaranteed approval?

No. They have higher approval chances but still require final verification.

Do pre-approved offers affect CIBIL score?

No, unless you submit the final application.

How long does approval take?

Many pre-approved cards are approved instantly or within 24 hours.

Can I get a pre-approved card with low credit score?

It is less common, but possible if you have strong banking history.

Conclusion: Pre-approved credit card offers are not random promotions. Banks carefully analyze your credit score, banking relationship, spending habits, and financial stability before selecting you. Maintaining strong financial discipline and consistent account activity significantly increases your chances of receiving instant approval offers with better benefits.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Credit card approvals, benefits, and eligibility criteria vary by bank policies, so readers should verify details directly with the issuing bank before accepting any offer.